How to Read an SEC Form 4: A Plain-English Guide to Insider Trading Filings

Corporate insiders are required to tell you when they buy or sell shares in their own company. Here’s how to actually read those filings — with real examples from Apple, NeurAxis, and Tectonic Therapeutic.

What Is a Form 4?

When a corporate officer, director, or major shareholder buys or sells stock in their own company, the SEC requires them to publicly disclose it. That disclosure is called a Form 4— formally titled the “Statement of Changes in Beneficial Ownership of Securities.”

This requirement comes from Section 16 of the Securities Exchange Act of 1934, one of the foundational laws governing U.S. stock markets. The logic is simple: people running a company know more about its prospects than you do. If they’re putting their own money in — or pulling it out — that’s information worth knowing.

Roughly 150,000 to 200,000 Form 4 filings hit the SEC’s EDGAR database every year. That’s a lot of data. The challenge isn’t finding insider filings — it’s knowing what they actually mean when you read one.

Who Has to File a Form 4?

Three categories of people are required to file:

Corporate officers— the C-suite and senior VPs. Think CEO, CFO, COO, General Counsel, and any other executive the company designates as a Section 16 officer.

Directors— every member of the company’s board of directors.

10% beneficial owners— anyone (person or entity) who owns more than 10% of any class of the company’s equity securities.

The filing deadline is tight: two business days after the transaction. If a CEO sells shares on Monday, the Form 4 must be filed by end of day Wednesday. This keeps the information reasonably fresh for investors like you.

The Anatomy of a Form 4

When you open a Form 4 on EDGAR, it looks like a government form from the 1990s — because it basically is. But there’s a clear structure once you know what to look for. Here’s what each section tells you.

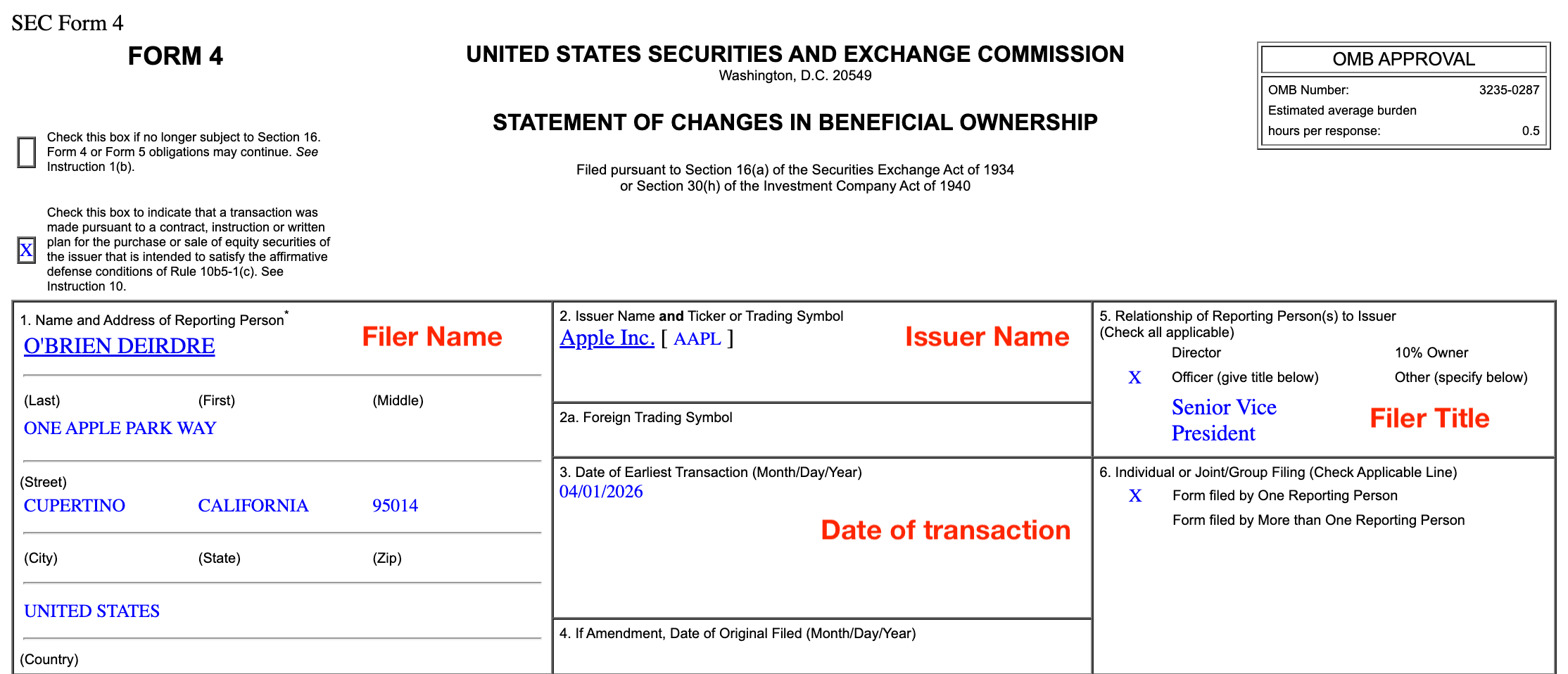

The Header: Who and What Company

The top of the form identifies the issuer (the company whose stock was traded) and the reporting person(the insider who made the trade). You’ll see the company name, its ticker symbol, and the insider’s name, title, and relationship to the company — whether they’re an officer, director, or 10% owner.

The header of a real Form 4 filing — Apple’s Deirdre O’Brien, filed April 3, 2026. Key fields annotated in red.

Table I: Non-Derivative Securities

This is where the straightforward action lives. Table I shows direct transactions in the company’s common stock — purchases, sales, awards, and similar. Each row is a separate transaction and tells you the date, the transaction code (more on this in a moment), how many shares, the price per share, and how many shares the insider owns after the transaction.

Table I from O’Brien’s Form 4: an RSU vesting (Code M), tax withholding (Code F), and open-market sales (Code S) across April 1–2, 2026.

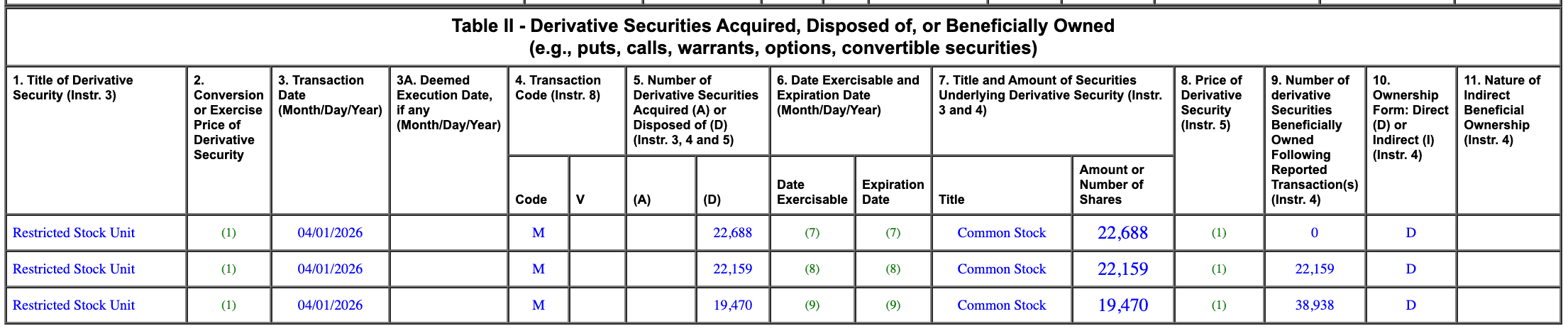

Table II: Derivative Securities

This is where things like stock options, restricted stock units (RSUs), warrants, and convertible securities show up. Derivative securities give the insider the right to acquire stock in the future under certain conditions. When an executive exercises stock options, for example, it shows here. Table II tracks the derivative security title, exercise price, number of shares, and the underlying common stock those derivatives convert into.

Table II from the same filing: three RSU grants (from 2021, 2022, and 2023) vesting on April 1, 2026, converting into Common Stock.

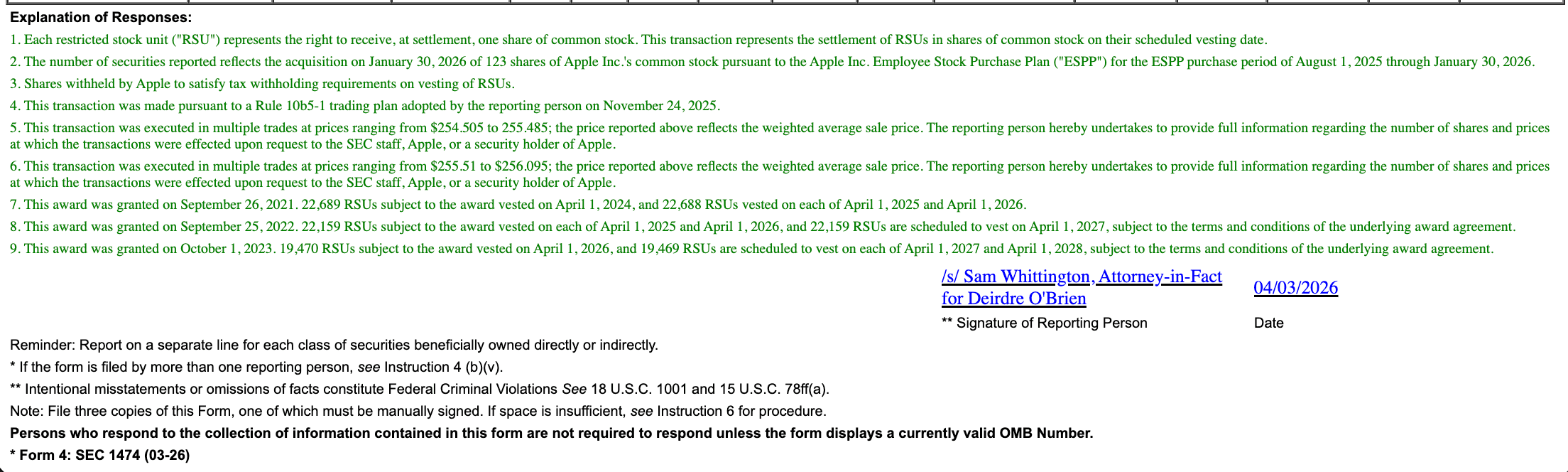

Footnotes

Don’t skip the footnotes. They contain critical context — whether the trade was part of a pre-planned 10b5-1 trading plan, when stock options or RSUs were originally granted, whether shares were withheld for taxes, and whether reported prices are averages of multiple trades. Footnotes often tell you more about the why than the tables do.

The footnotes from O’Brien’s filing — revealing the 10b5-1 plan, tax withholding details, weighted-average sale prices, and original RSU grant dates. This is where the real context lives.

Signature and Filing Date

At the bottom you’ll find who signed the filing (often an attorney-in-fact on behalf of the insider) and the date it was filed. Compare the filing date to the transaction date — if there’s a significant gap, the insider may have missed the 2-business-day deadline, which itself is worth noting.

Transaction Codes: The Rosetta Stone of Form 4

Every transaction on a Form 4 has a single-letter code that tells you what kind of transaction it was. This is arguably the most important thing to understand, because not all insider transactions carry the same meaning.

Real Example: Apple’s Deirdre O’Brien

View the original filing on SEC EDGAR →

Let’s walk through an actual Form 4 from the SEC’s EDGAR database. On April 3, 2026, Apple filed a Form 4 for Deirdre O’Brien, Senior Vice President of Retail + People. The filing covers transactions on April 1–2, 2026. Here’s what it tells us, section by section.

Filing Header

Table I — Non-Derivative Transactions (Common Stock)

| Date | Code | Shares | Price | Shares After |

|---|---|---|---|---|

| Apr 1 | M — Vesting | 64,317 acquired | — | 201,127 |

| Apr 1 | S — Sale | 34,315 disposed | $255.63 | 166,812 |

| Apr 2 | S — Sale | 20,338 disposed | $255.12 | 146,474 |

| Apr 2 | S — Sale | 9,664 disposed | $255.82 | 136,810 |

Table II — Derivative Transactions (RSUs)

| Date | Security | Shares | Grant Date (from footnotes) |

|---|---|---|---|

| Apr 1 | Restricted Stock Unit | 22,688 disposed | September 26, 2021 |

| Apr 1 | Restricted Stock Unit | 22,159 disposed | September 25, 2022 |

| Apr 1 | Restricted Stock Unit | 19,470 disposed | October 1, 2023 |

What the Footnotes Tell Us

The footnotes on this filing are where the real story lives:

RSU vesting across three grants:O’Brien had RSUs from three separate annual grants (2021, 2022, and 2023) that all vested on April 1, 2026. Those 64,317 shares that appeared in Table I as “acquired” are the total common stock she received when those RSUs converted.

Tax withholding:A footnote explains that some shares were withheld by Apple to satisfy tax obligations on the RSU vesting. When RSUs vest, the IRS treats that as income, so companies typically withhold a portion of shares to cover the tax bill. This is automatic — the insider doesn’t choose to do it.

Rule 10b5-1 plan:The sales were executed under a pre-arranged trading plan. This means O’Brien set up the sales months in advance, not in response to any recent news or internal information.

Weighted-average prices:The reported sale prices are weighted averages — one footnote notes trades ranged from $254.505 to $255.485 in a single batch. This is normal for large orders that execute in multiple pieces throughout the day.

Real Example: NeurAxis Director Buys $1M — Stock Rallies 112%

View the original filing on SEC EDGAR →

Now let’s look at the opposite pattern — and the one that gets investors most excited. On December 29, 2025, Neuraxis Inc. filed a Form 4 for Gil Aharon, a director of the company. This filing covers a transaction on December 23, 2025.

The context matters here. NeurAxis (NRXS) is a small-cap medical device company based in Carmel, Indiana. They make a non-invasive neuromodulation device called IB-Stim, FDA-cleared for treating functional abdominal pain and related conditions. In the days leading up to the purchase, the stock had been trading around $3.22. A few key catalysts were brewing: on December 19, a major insurer had expanded coverage to 45 million additional lives (bringing total covered lives to 100 million), and a landmark Category I CPT code— the gold standard for permanent insurance reimbursement — was set to take effect on January 1, 2026. The stock was starting to move, but hadn’t broken out yet.

On December 23, Aharon stepped in with a $1 million open-market purchase.

Filing Header

Table I — One Clean Transaction

| Date | Code | Shares | Price | Ownership | Shares After |

|---|---|---|---|---|---|

| Dec 23 | P — Purchase | 286,138 acquired | $3.52 | Indirect | 286,138 |

Total investment: 286,138 shares × $3.52 = $1,007,206. This was Aharon’s first position in the company — he went from zero shares to 286,138.

Table II — Empty

No derivative transactions. No options, no RSUs, no warrants. This is a pure open-market cash purchase — as clean as a Form 4 gets.

What the Footnotes Tell Us

Purchased via Rosalind Master Fund L.P.:The footnotes reveal this purchase was made through Rosalind Master Fund L.P., with Rosalind Advisors, Inc. acting as the fund’s advisor. Aharon is associated with the fund. This is indirect ownership — common when a director also manages or is affiliated with an investment fund.

Disclaimer of beneficial ownership:A standard footnote states that Aharon disclaims beneficial ownership “except to the extent of his or her pecuniary interest.” This is boilerplate legal language you’ll see on any filing where shares are held through a fund or trust.

No 10b5-1 plan:The 10b5-1 checkbox is empty. This was a discretionary, timely purchase — not something arranged months in advance.

What Happened to the Stock After?

This is where it gets interesting. Here’s the timeline:

| Date | Event | NRXS Price | Gain from $3.52 |

|---|---|---|---|

| Dec 19 | Pre-purchase (insurer coverage expansion announced) | $3.22 | — |

| Dec 23 | Aharon buys 286,138 shares | $3.52 | Entry |

| Dec 31 | Year-end | $4.54 | +29% |

| Jan 1 | Category I CPT code takes effect | — | — |

| Early Jan | CPT code milestone announced | ~$4.68 | +33% |

| Mar 20 | All-time high | $7.97 | +126% |

Let’s put that in dollar terms. Aharon’s $1 million investment was worth roughly $1.33 million within two weeks (+33%), and peaked at approximately $2.28 million by March 20— a gain of over $1.2 million in under three months. Craig-Hallum, an investment bank covering the stock, raised their price target from $8 to $13 during this period.

The stock was being driven by real fundamental catalysts — the Category I CPT code (effective January 1, 2026) established a permanent reimbursement pathway, the insurer coverage expansion dramatically increased the addressable market, and a Veterans Affairs contract added federal revenue. The insider knew these catalysts were coming and put significant capital behind that conviction.

Real Example: Tectonic Therapeutic CFO Buys a 41% Crash

View the original filing on SEC EDGAR →

Here’s another pattern worth studying — the CFO who bought the crash. On February 11, 2026, Tectonic Therapeutic filed a Form 4 for Daniel Lochner, the company’s Chief Financial Officer. The filing covers a purchase made on February 10, 2026.

Tectonic Therapeutic (TECX) is a clinical-stage biotech company developing GPCR-targeted biologic medicines. On February 9, the stock closed at $24.83. The next morning, it opened at roughly $14.70 — a 41% gap-down crash. While other investors were panic-selling, the company’s CFO — the person who knows the balance sheet better than anyone — walked in and bought 6,000 shares.

Filing Header

Table I — One Clean Transaction

| Date | Code | Shares | Price | Ownership | Shares After |

|---|---|---|---|---|---|

| Feb 10 | P — Purchase | 6,000 acquired | $21.61 | Direct | 32,044 |

Total investment: 6,000 shares × $21.61 = $129,660. Lochner already held 26,044 shares before this purchase — he increased his position by 23%.

Table II — Empty

No derivative transactions. Clean open-market purchase.

What the Footnotes Tell Us

Weighted-average price:The $21.61 is a weighted average from multiple transactions executed throughout the day. On a crash day with extreme volatility, Lochner was buying in pieces as the price stabilized — a disciplined approach.

No 10b5-1 plan:Empty checkbox. This was entirely discretionary. The CFO saw a 41% crash, decided on the spot that it was overdone, and put $130K of his own money behind that view. Signed by Lochner himself — no attorney-in-fact, no intermediary.

What Happened to the Stock After?

| Date | Event | TECX Price | Gain from $21.61 |

|---|---|---|---|

| Feb 9 | Day before crash (close) | $24.83 | — |

| Feb 10 | Crash day (intraday low ~$14.70, -41%) | ~$14.70 | — |

| Feb 10 | Lochner buys 6,000 shares | $21.61 | Entry |

| Feb 26 | Earnings beat (EPS -$1.03 vs. -$1.11 est.) | ~$24 | +11% |

| Mar 7–9 | New 52-week high | ~$34 | +57% |

| Early Apr | Current range | ~$29 | +35% |

Lochner’s $129,660 investment was worth roughly $204,000 at the March peak — a gain of about $74,000 in under a month. Even after pulling back, his position was still up 35% by early April. The recovery was supported by an earnings beat on February 26 and a KOL event showcasing their TX2100 pipeline program. Analysts at Lifesci Capital upgraded the stock to “Strong Buy” just days before Lochner’s purchase, and the consensus price target among covering analysts sits at $81.50 — nearly 3x the current price.

Three examples, three very different stories. O’Brien’s Apple filing was routine compensation management — no signal. Aharon’s NeurAxis filing was a director opening a $1M position ahead of catalysts — strong signal, 112% gain. Lochner’s Tectonic filing was a CFO buying a crash with his own cash — strong signal, 57% peak gain. The difference between noise and signal on a Form 4 is everything.

What’s a Rule 10b5-1 Plan?

You’ll see this referenced in footnotes constantly, so it’s worth understanding. A 10b5-1 plan is a pre-arranged trading schedule that insiders set up in advance — typically when they don’t possess any material non-public information.

The plan specifies in advance how many shares to sell, at what price thresholds, and on what dates. Once it’s in place, the trades execute automatically. The insider can’t change the plan based on information they later learn.

Why does this exist? It gives insiders a legal safe harbor. Without 10b5-1 plans, executives would face an impossible dilemma: they always have some degree of non-public information, so when could they ever sell stock? These plans solve that by separating the decision to sell from the execution of the sale by months.

The SEC tightened the rules in December 2022, requiring a minimum “cooling-off period” of at least 90 days between adopting a plan and the first trade executing, and limiting single-trade plans to one per 12-month period. The forms now include a checkbox indicating whether a transaction was made under a 10b5-1 plan.

Does Insider Trading Actually Predict Stock Movements?

This is what everyone really wants to know. The academic research is surprisingly clear — and nuanced.

Insider buying is a strong signal.Studies spanning decades show that stocks bought by insiders (Code P transactions) outperform the broad market by roughly 6% to 10% annually. One widely cited study found that aggregate insider net purchases predicted up to 60% of variation in one-year-ahead stock returns. When an executive voluntarily puts their own cash into the stock, they’re usually right.

Insider selling is much noisier.People sell for all sorts of reasons that have nothing to do with the company’s prospects — buying a house, paying taxes, diversifying their portfolio, funding a divorce. Research published in the Financial Analysts Journal found that small sales (those representing a small percentage of the insider’s total holdings) actually correlated with positive future returns, not negative ones.

But cluster selling matters. When multiple insiders at the same company sell around the same time, that carries a significantly stronger negative signal. One person selling could mean anything. Five people selling in the same month tells a different story.

Context is everything.The most predictive signals come from large, non-routine transactions by senior insiders — particularly the CEO and CFO. Small transactions from lower-ranking officers are statistically closer to noise.

5 Common Mistakes When Reading Form 4s

1. Treating all transactions equally. A Code F (tax withholding) and a Code P (open-market purchase) look similar in the table but mean completely different things. Always check the transaction code first.

2. Panicking at large sales numbers.A headline like “CEO sells $50 million in stock” sounds dramatic until you realize they still hold $400 million in shares and the sale was under a 10b5-1 plan filed six months ago. Always look at what percentage of their holdings the sale represents.

3. Ignoring the footnotes. The footnotes contain the context that turns raw data into actual insight. Was it a pre-planned sale? Were shares withheld for taxes? Was the price a weighted average? The footnotes tell you.

4. Looking at one filing in isolation.A single Form 4 is a snapshot. The real signal comes from patterns — is this insider consistently buying over months? Are multiple insiders at the same company all selling? Track the trend, not the individual filing.

5. Confusing legal insider trading with illegal insider trading.Form 4 is the mechanism for legal, disclosed trading. If someone were trading on illegal inside information, they wouldn’t be filing a form about it.

How to Find Form 4 Filings

All Form 4 filings are publicly available on the SEC’s EDGAR database at sec.gov/edgar. You can search by company name, ticker symbol, or the insider’s name. Each filing links to the HTML and XML versions of the form.

The challenge? EDGAR is functional but not user-friendly. The interface hasn’t been meaningfully updated in years. Finding, reading, and cross-referencing filings across multiple companies is time-consuming. The XML data is powerful but not designed for casual investors to parse. And making sense of the transaction codes, footnotes, and derivative tables requires the kind of knowledge you just learned in this article.

Skip the XML. Get the signal.

MarketPeel distills SEC insider filings into clear, readable insights so you can spot meaningful insider activity without digging through EDGAR yourself. We flag the transactions that matter — open-market purchases, cluster selling, unusual activity — and filter out the noise of routine compensation transactions.

Try MarketPeel free →Sources & Further Reading

SEC — Exchange Act Section 16 and Related Rules

SEC — Form 4 Official Instructions

SEC — 2022 Amendments to Rule 10b5-1

SEC EDGAR — Apple Inc. Form 4 (Deirdre O’Brien, April 3, 2026)

SEC EDGAR — Neuraxis, Inc. Form 4 (Gil Aharon, December 29, 2025)

SEC EDGAR — Tectonic Therapeutic, Inc. Form 4 (Daniel Lochner, February 11, 2026)

SEC Investor Bulletin — Forms 3, 4, and 5

2IQ Research — Profiting From Insider Transactions: Academic Review

NASPP — Section 16 Basics of Forms 3, 4, and 5